There is a question every pharma company building an oncology pipeline eventually has to answer honestly: do we build this manufacturing capability ourselves, or do we find someone who already has it?

Building it yourself means years of facility construction, regulatory qualification, hiring specialized talent, and locking up capital that could have gone into your pipeline. And that is before the first batch rolls off the line. For oncology specifically, where containment infrastructure, regulatory approvals, and formulation expertise have to exist together before you can make a single commercial unit, the cost and timeline of going in-house are genuinely prohibitive for most organizations.

That is why the most consistent strategic move in the pharmaceutical industry right now is the one toward specialized oncology CDMO partners in India. Not as a cost-cutting shortcut, but as a deliberate decision to access capabilities that take fifteen years and hundreds of millions of dollars to build, without bearing the cost of building them.

This piece makes the case for why that decision, when made with the right partner, genuinely changes a company’s competitive position in the oncology market.

The Market Context: Why This Decision Matters More Now Than Before

The global CDMO market is projected to grow from approximately USD 255 billion in 2025 to over USD 465 billion by 2032, driven by the rise of complex biologics, cell and gene therapies, and geopolitical forces actively reshaping global supply chains.

Two forces in particular are accelerating that shift toward India right now.

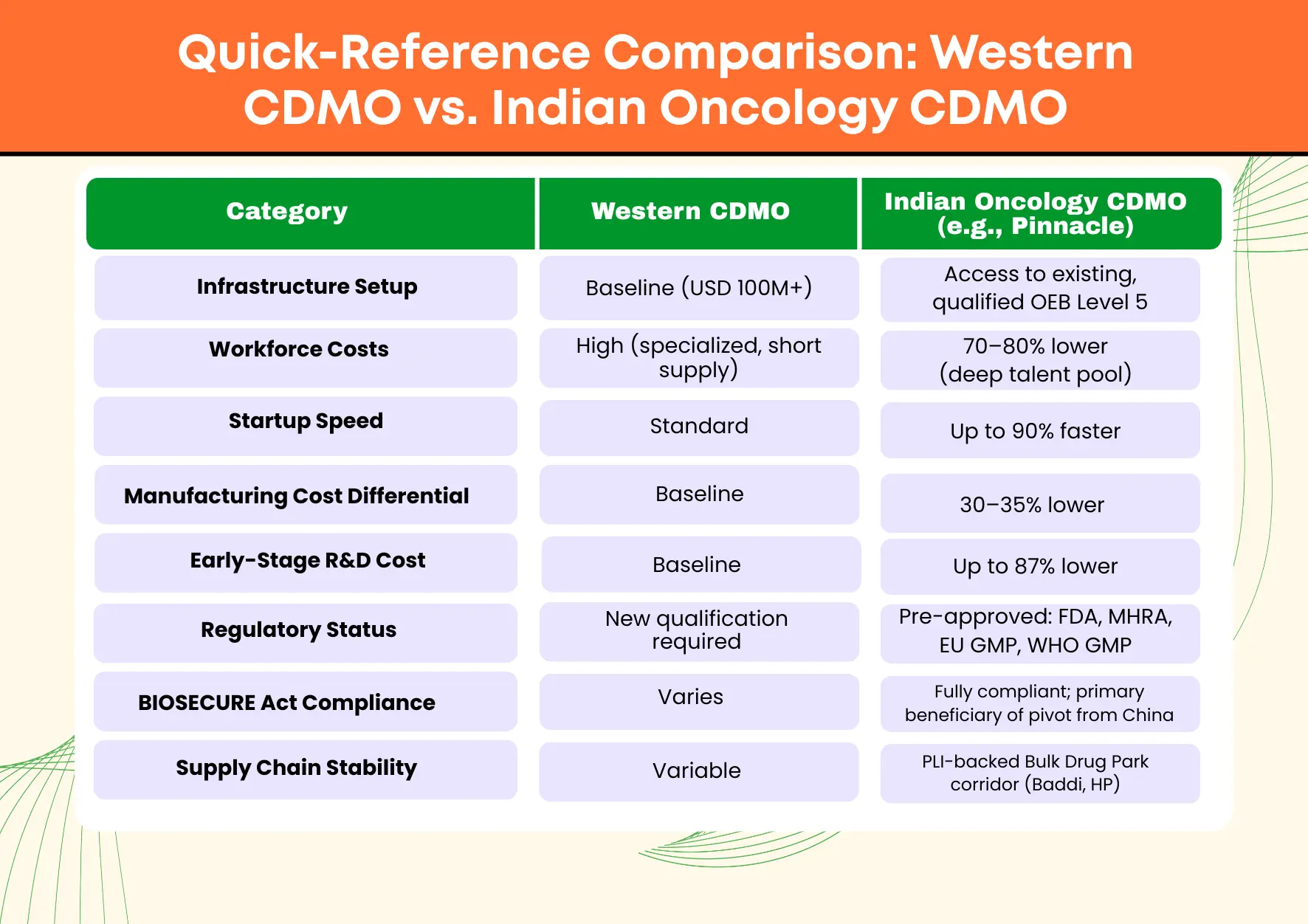

The first is legislative. The US BIOSECURE Act (H.R. 8333 / S. 3558), which restricts US federal agencies from contracting with designated China-based biotechs, finalized its list of companies of concern in early 2026. Global pharma companies are now actively migrating oncology projects away from affected Chinese CDMOs to avoid federal contract prohibitions — and India is the primary beneficiary of that migration. Indian CDMOs offer startup timelines running up to 90 percent faster than Western alternatives, workforce costs running 70 to 80 percent lower, and infrastructure setup costs running 85 percent lower.

The second is structural. The Indian CDMO segment is outpacing the global market’s growth rate. Valued at approximately USD 23.3 billion in 2026, the Indian CDMO market is projected to reach USD 55.5 billion by 2033, growing at a 13.2 percent CAGR — nearly double the global average. PharmaSource Oncology remains the dominant therapeutic area within that segment, accounting for approximately 30 percent of market share.

Reinforcing this further, India’s government-backed Production Linked Incentive (PLI) schemes have specifically designated the Himachal Pradesh corridor — home to Baddi, one of India’s largest pharmaceutical manufacturing clusters — as a priority Bulk Drug Park zone. For OEB Level 5 oncology manufacturing, this translates into policy-backed supply chain stability, infrastructure investment support, and a deep regional talent pool of qualified pharmaceutical scientists and GMP-trained operators.

The companies building long-term oncology programs today are not deciding between India and a better option. They are deciding between India and a more expensive, slower, or geopolitically riskier one.

What an Oncology CDMO in India Actually Gives You

A. Infrastructure You Cannot Justify Building Yourself

Setting up an OEB Level 5 oncology containment facility from scratch costs between USD 50 million and USD 100 million depending on scale, and that number does not include the timeline for regulatory qualification. Most pharmaceutical companies, including mid-size and even large-cap organizations, have no rational basis for making that capital commitment when they can access the same infrastructure through a CDMO partnership.

The leading CDMO pharma companies in India have already made that investment, already passed the regulatory inspections that validate it, and are ready to deploy it on your program without the three-to-five-year runway of building equivalent capability in-house. For a company whose advantage lies in drug discovery, clinical development, and commercialization, this is not outsourcing. It is specialization by design.

B. Regulatory Approvals Across Multiple Markets, Already in Place

This is the advantage that takes longest to build and is hardest to replicate. A serious oncology CDMO with concurrent US FDA, EU GMP, UK MHRA, and WHO GMP approvals has been through independent adversarial inspections across four of the world’s most demanding regulatory frameworks. Each approval represents inspectors walking the production floor, reviewing deviation logs, checking batch manufacturing records against SOPs, and confirming that the quality systems the facility claims to operate are the ones it actually uses.

When your molecule needs to enter the US, European, and emerging markets simultaneously, having a manufacturing partner with those approvals already in place removes one of the most time-consuming and uncertain variables in your launch timeline. You are not waiting for your partner to earn approvals your product needs. They already have them.

C. 30–40% Lower Manufacturing Costs — and Up to 87% Lower R&D Costs

This number gets cited often enough that it starts to sound like marketing. It is not. On average, oncology manufacturing in India costs 30 to 35 percent less compared to Western facilities, driven by structurally lower labor costs, facility operating costs, and GMP-compliant consumable pricing. For early-stage R&D specifically, the differential is substantially larger — recent data indicates R&D expenses in India can run up to 87 percent lower than in developed markets, reflecting the structural difference in scientific labor costs and facility overhead at the development stage. Pinnacle Life Science

None of that reflects lower quality. It reflects a different cost structure in a country that has built a world-class pharmaceutical manufacturing ecosystem over three decades.

For an oncology program that will spend years in clinical development before generating a single dollar of commercial revenue, that saving is not a rounding error. It is the difference between a program that is financially viable and one that is not.

D. End-to-End CDMO Services Under One Roof

The operational benefit of a true oncology CDMO is continuity. When formulation development, clinical trial material manufacturing, regulatory dossier preparation, technology transfer, and commercial production all happen with the same partner, there are no handoffs between vendors where data gets lost, processes get reinterpreted, or timelines get renegotiated.

A significant delay in manufacturing of clinical trial materials can push back a pivotal study, and a delay in commercial production means a delay in market entry. In the pharmaceutical industry, where products have a finite period of patent-protected market exclusivity, every day of delay is a day of lost revenue at peak prices. Drug Patent Watch

This is where the CDMO model earns its cost premium over a simple toll manufacturer. The value is not just in what each stage costs. It is in what the transitions between stages do not cost you when they are managed by a single integrated partner.

E. Modified-Release Capability for Precision Oncology Dosing

The shift toward precision medicine in 2026 has elevated modified-release formulation from a secondary capability to a front-line requirement. Precision oncology increasingly demands dosing regimens engineered to maintain therapeutic concentrations over defined windows while minimizing peak-dose toxicity — outcomes that depend entirely on controlled-release formulation design. A CDMO without genuine modified-release R&D capability cannot support this direction. For programs aligned with personalized cancer therapy, verify this capability explicitly before engaging any manufacturing partner.

Quick-Reference Comparison: Western CDMO vs. Indian Oncology CDMO

| Category | Western CDMO | Indian Oncology CDMO (e.g., Pinnacle) |

| Infrastructure Setup | Baseline (USD 100M+) | Access to existing, qualified OEB Level 5 |

| Workforce Costs | High (specialized, short supply) | 70–80% lower (deep talent pool) |

| Startup Speed | Standard | Up to 90% faster |

| Manufacturing Cost Differential | Baseline | 30–35% lower |

| Early-Stage R&D Cost | Baseline | Up to 87% lower |

| Regulatory Status | New qualification required | Pre-approved: FDA, MHRA, EU GMP, WHO GMP |

| BIOSECURE Act Compliance | Varies | Fully compliant; primary beneficiary of pivot from China |

| Supply Chain Stability | Variable | PLI-backed Bulk Drug Park corridor (Baddi, HP) |

What Separates a Strategic CDMO Partnership from a Vendor Relationship

Most companies that have been through a failed or frustrating contract manufacturing experience describe the same problem. They treated the CDMO as a vendor and got vendor-level engagement. The ones that consistently get the most out of these partnerships treat them as strategic relationships from day one.

Transparency Over the Program, Not Just the Purchase Order

A CDMO partner worth having will tell you when a formulation approach is not going to work before you have spent three months and a significant budget finding out the hard way. That kind of technical transparency requires a relationship where the partner has a stake in your program’s success, not just in billing the current milestone.

Regulatory Alignment from the Start

Strong regulatory support reduces the risk of delays and non-compliance. Ask specifically about dossier preparation capability, regulatory filing support, audit readiness, and country-specific compliance for each market you intend to enter. Pinnacle Life Science The best CDMO companies embed regulatory affairs into the development and manufacturing relationship from the beginning, so submissions are built on the same documentation the manufacturing team is already generating. The ICH Common Technical Document (CTD) framework is the standard reference for understanding why dossier preparation requires specialist integration rather than a separate workstream.

Capacity That Can Actually Scale

A partner with 3 billion tablets of annual production capacity and proven scale-up experience is a different proposition from one that handles your Phase III supply beautifully and then cannot keep pace with commercial demand. Verify that your CDMO can handle both ends of the volume spectrum with the same quality systems.

Why Pinnacle Life Science Is Built for This Relationship

Pinnacle Life Science operates as a dedicated oncology CDMO and pharma contract manufacturer from cGMP-compliant facilities in Baddi, Himachal Pradesh, as part of the Aarti Group — a diversified chemical and pharmaceutical conglomerate with revenues exceeding USD 1.5 billion. That parent-company relationship provides deep backward integration into API and specialty chemical supply chains, directly addressing the raw material vulnerabilities that BIOSECURE Act-driven supply chain reorganisation has brought into sharp focus.

The oncology unit runs at OEB Level 5 containment, with concurrent approvals from the US FDA, UK MHRA, EU GMP, WHO GMP, MCAZ Zimbabwe, and DIGEMID Latin America — concurrent approvals across the same manufacturing operation, not distributed across different sites.

In-house R&D covers formulation development, modified-release product engineering for precision oncology dosing requirements, and patent non-infringing generics. The Regulatory and IPR Cell prepares CTD-formatted ANDAs and dossiers for regulated market submissions. With 3 billion tablets and 300 million capsules produced annually for 400-plus clients across 90-plus countries, Pinnacle’s scale and specialization exist at the same time rather than as a tradeoff.

The infrastructure page covers containment capability and facility detail. The manufacturing and CDMO services overview covers development through commercial supply.

Frequently Asked Questions

What is an oncology CDMO and why does it matter for pharma companies?

An oncology CDMO is a contract development and manufacturing organization that specializes in cancer drug development and production. It covers formulation R&D, clinical trial supply, regulatory affairs, and commercial manufacturing under one structure. For pharma companies without in-house oncology manufacturing capability, a CDMO partner provides access to OEB-level containment, multi-agency regulatory approvals, and formulation expertise that would take many years and hundreds of millions of dollars to build independently.

How much can a pharma company actually save by partnering with an Indian oncology CDMO?

Oncology manufacturing in India typically costs 30 to 35 percent less than equivalent programs in Western facilities. For early-stage R&D, the differential can reach up to 87 percent, driven by structurally lower scientific labor and facility overhead costs. The savings come from a different cost structure in a country that has built a world-class pharmaceutical ecosystem over three decades — not from lower quality standards.

What CDMO services should an oncology program expect from a quality Indian partner?

Pre-formulation and formulation development, analytical method development, clinical trial material manufacturing, technology transfer, regulatory dossier preparation for multiple markets including CTD and ANDA filings, and commercial-scale manufacturing. Some oncology CDMOs also offer API backward integration, which adds supply chain resilience to the partnership.

How does the BIOSECURE Act affect oncology CDMO partnerships with India?

The BIOSECURE Act (H.R. 8333 / S. 3558) restricts US federal agencies from working with designated China-based biotechs. As of early 2026, the act has finalized its companies of concern list, pushing global pharma to migrate oncology manufacturing to compliant alternatives. India has become the primary beneficiary, with established US FDA and EU GMP approvals making Indian CDMOs the natural destination for redirected programs.

What questions should I ask before choosing between CDMO companies for an oncology program?

Ask about their OEB containment level and the third-party SMEPAC testing documentation that supports it. Ask for their inspection history with the FDA and MHRA specifically. Ask how they handle deviations and CAPAs. Ask for case studies on technology transfer from clinical to commercial scale. Ask whether their regulatory affairs function is genuinely integrated or separately contracted. And ask specifically about their experience with the molecule class and dosage form your program requires.

Is pharma contract manufacturing in India suitable for regulated market launches?

Yes. The leading pharmaceutical contract manufacturers in India hold concurrent approvals from the US FDA, EU GMP, and UK MHRA, enabling product supply directly into regulated markets in North America, Europe, and beyond. Many also carry ANVISA approval for Brazil and WHO GMP certification for multilateral procurement markets across Africa and Southeast Asia.

The Final Verdict

The decision to partner with a specialist oncology CDMO is not a procurement decision. It is a strategic one that determines how fast your program moves, how much it costs, and whether your manufacturing partner’s quality record strengthens or complicates your regulatory submissions. The companies that treat it that way consistently get better outcomes than the ones that treat it as vendor selection.

Contact Pinnacle Life Science to discuss how an oncology CDMO partnership can support your development and commercial manufacturing program.

Oncology Medicine Manufacturers in India: What the Numbers Don’t Tell You

India has some genuinely strong oncology medicine manufacturers, but they’re not all built the same. Here’s what actually matters when you’re trying to find a credible partner in cancer drug manufacturing.

CDMO Companies in India: What to Know Before You Partner

India’s CDMO sector is growing fast, and for good reason. But not every partner is built the same. Here’s a practical, no-jargon guide to understanding what CDMO companies in India actually offer and how to choose wisely.

CDMO Full Form: What Is a CDMO in Pharma and How Does It Actually Work?

CDMO stands for Contract Development and Manufacturing Organization. But knowing the full form is just the starting point. Here’s what CDMOs actually do, why they matter in pharma, and how they’re different from CMOs and CROs.